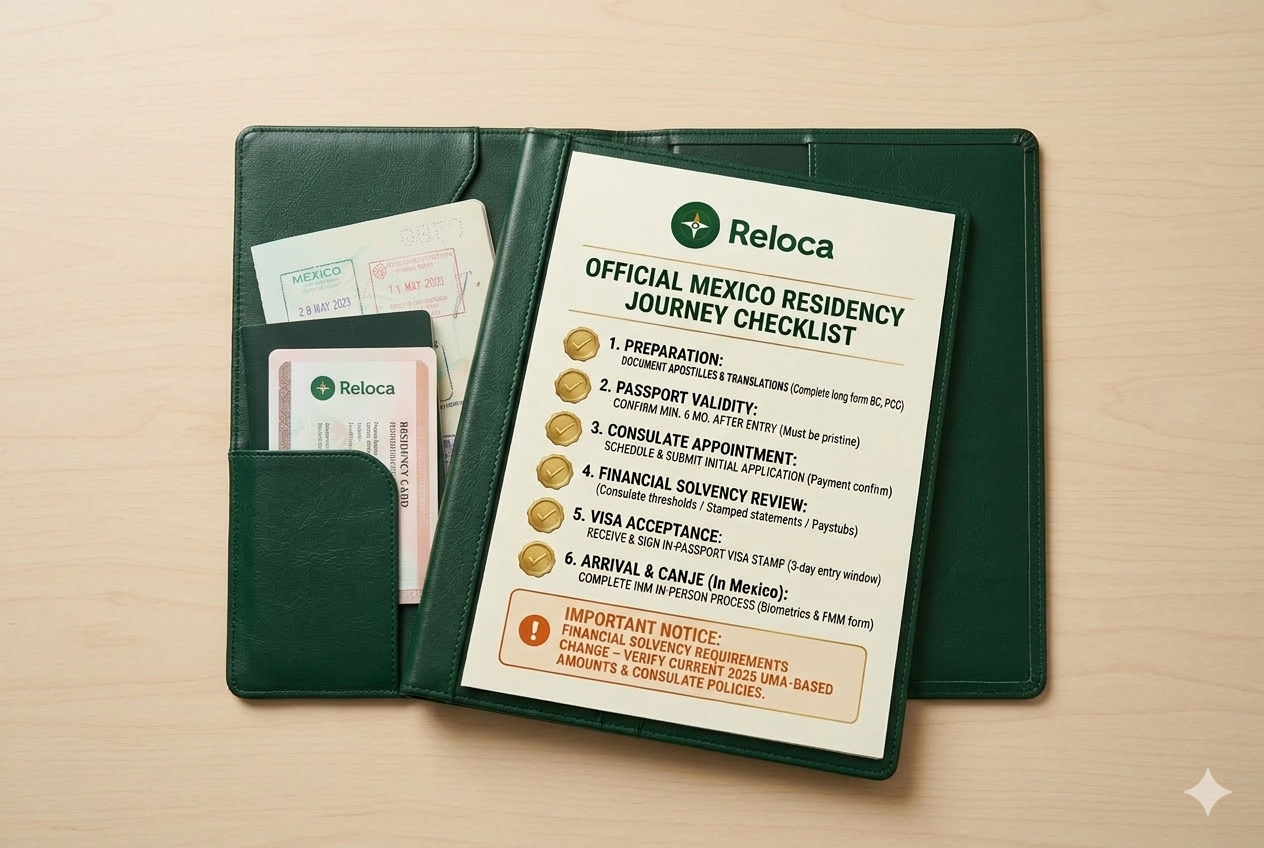

Understanding what bank account documents are needed for Mexico residency is more complicated than most people expect, because you are actually dealing with two completely separate challenges. First, you need the right financial documents to convince the consulate to approve your visa. Then, after you arrive in Mexico with your residency card in hand, you need a different set of documents to open a local bank account. Both steps have their quirks, and mixing them up is one of the most common reasons applications get delayed or rejected.

Key Takeaways

- You do not need a Mexican bank account to apply for residency. You use your existing US or Canadian bank statements at the consulate stage, get approved, and only then open a local Mexican account after receiving your resident card.

- For the consulate application, you must provide full detailed statements covering the six or twelve months before your application date, showing every transaction and balance. Summary or abridged pages are not accepted.

- The 2026 financial thresholds are approximately US$4,400 per month in income or US$74,000 in savings for temporary residency, and US$7,400 per month or US$298,000 in savings for permanent residency. Canadian equivalents are CA$6,461 per month or CA$108,894 in savings for temporary residency, and CA$10,832 per month or CA$435,672 for permanent residency.

- To open a Mexican bank account after receiving your resident card, you must appear in person at a branch with your passport, resident card, proof of Mexican address, CURP, and a Mexican mobile phone number. Online account opening is not available to foreign residents.

- Statement format requirements vary by consulate, with some requiring original paper statements stamped by your bank and others accepting PDF printouts. Any financial documents used at an immigration office inside Mexico must be translated into Spanish by a certified translator.

The Chicken-and-Egg Problem: Residency vs. a Mexican Bank Account

Here is the frustrating reality: most Mexican banks require you to already have legal residency status before they will open an account for you. That means they want to see your Residente Temporal or Residente Permanente card before anything else. But to get that residency card, you need to show the consulate bank statements, usually from a foreign account.

So if you are wondering whether you need a Mexican bank account before applying for residency, the short answer is no. You apply for residency using your US or Canadian bank statements, get approved, move to Mexico, receive your resident card, and then open a local account. Most expats keep their foreign accounts active throughout the entire process, and many keep them indefinitely.

This two-stage reality is worth keeping in mind as you read through the rest of this guide. The documents you need at each stage are quite different.

Bank Account Documents Required When Applying for Mexico Residency (Stage One)

At the consulate stage, the documents you need from your bank are straightforward in concept but fussy in execution. Consulates want to see that you have enough money coming in or sitting in savings to support yourself in Mexico without working locally. Your bank statements are the primary way you prove this.

What Your Bank Statements Must Show

Consulates require full, detailed account statements covering the entire qualifying period, which is either the six or twelve months immediately before your application date. Some consulates ask for six months, others prefer twelve. Check with your specific consulate before assembling your package.

The key word here is "detailed." Most consulates and all immigration offices inside Mexico will reject abridged statements or summary pages. They want to see every transaction, every deposit, and every balance across the full period. If your bank's website generates a one-page summary, that is not going to work.

What Types of Accounts Qualify

You can use checking accounts, savings accounts, 401(k)s, IRAs, RRSPs, and other investment accounts to demonstrate financial solvency. The key requirement is that the funds are liquid and clearly denominated in a recognized currency. What does not work: real estate equity, cryptocurrency holdings, precious metals, or stock positions that are not held as cash or cash equivalents in a traditional financial institution. Consulates want to see actual money in actual accounts.

If you are combining income from multiple accounts, most consulates will allow you to present statements from two or more accounts as long as all of them are in your name. None of those accounts can be cryptocurrency wallets or exchanges.

The 2026 Financial Thresholds You Need to Hit

For temporary residency in 2026, you need to show either approximately US$4,400 per month in net income consistently over the qualifying period, or roughly US$74,000 in total savings and investments. For permanent residency, those numbers jump significantly: around US$7,400 per month in income, or approximately US$298,000 in savings.

These figures can vary by consulate, typically within a range of plus or minus five to ten percent. For a deeper look at how these thresholds work and which path makes more sense for your situation, the Mexico temporary residency income requirements guide breaks it all down clearly. And if you are closer to the permanent residency threshold, the Mexico permanent residency financial requirements guide is worth reading before your appointment.

Document Format: Originals, PDFs, and Translations

This is where things get inconsistent, and it is worth calling your specific consulate ahead of time. Some consulates insist on original paper statements stamped by your bank branch or accompanied by a signed letter confirming you are the account holder. Others accept clean PDF printouts without any fuss at all. There is no universal rule here, just consulate-by-consulate preferences.

If you are completing your canje (the INM process inside Mexico to convert your consulate visa into a resident card), your financial statements will need to be translated into Spanish by a certified translator. This applies to any immigration office appointment inside Mexico, not just the consulate stage.

Special Rules for Couples

If you and a partner are applying together using a joint account, you do not need to show double the required balance. The standard threshold applies once to the household. This is a meaningful advantage for couples where one partner is the primary account holder.

Bank Account Documents Needed to Open a Mexican Account (Stage Two)

Once you have your resident card, opening a local bank account becomes much easier. Here is what you will typically need to bring to the branch in person.

- Valid passport with a current, unexpired visa stamp

- Your resident card (Residente Temporal or Residente Permanente)

- Proof of address in Mexico, usually a recent utility bill in your name

- CURP (Unique Population Registry Code), which you receive after completing the INM process

- RFC (Federal Taxpayer Registry number), required by some banks but not all

- A Mexican mobile phone number, for account verification and SMS codes

- Minimum opening deposit, typically around MXN $800 to $1,000, which is roughly USD $40 to $50

One important thing to know: as a foreign resident, you cannot open a Mexican bank account online. You have to go into a branch in person. Set aside one to two hours for the visit. Some banks will issue your debit card on the spot; others will mail it to you within a few business days.

If you do not yet have your CURP or RFC sorted out, the guide to getting your CURP after residency approval and the guide to getting your RFC as a foreign resident will walk you through both processes step by step.

Best Banks for Expats in Mexico

The banks that expats use most consistently are BBVA Bancomer, Banorte, Banco Santander, and Citibanamex. BBVA tends to be the most expat-friendly, with English-speaking staff at larger branches in popular expat cities. That said, experiences vary a lot depending on which branch you visit and which staff member handles your account opening.

For a detailed look at what BBVA specifically requires from foreign residents, the BBVA account requirements for foreigners guide covers the current process and what to expect.

Common Mistakes That Lead to Rejection

A few errors come up again and again when people submit their bank account documents for residency applications, and most of them are entirely avoidable.

- Submitting summary statements instead of detailed ones. If the statement does not show every transaction and running balance, it is likely to be rejected. Always request full statements from your bank, not year-end summaries.

- Inconsistencies in your name or account details. If your bank statement shows "Robert Smith" but your passport says "Robert J. Smith," even a small discrepancy like that can create problems at some consulates. Make sure names match exactly across all documents.

- Using non-liquid assets as proof of solvency. Crypto, property appraisals, and precious metals do not count. Stick to cash accounts and recognized investment accounts.

- Forgetting certified translations for INM appointments. If you are filing inside Mexico, everything financial needs to be in Spanish from a certified translator.

- Not confirming your consulate's specific format preference. Some want originals, some accept PDFs. Do not assume.

The full breakdown of why Mexico residency visas get denied covers these issues and more, and it is worth reading before you finalize your document package.

Renewals: Do You Need to Resubmit Bank Documents?

Good news here: when you renew your temporary residency, you generally do not need to resubmit proof of economic solvency. The renewal process is simpler than the original application. However, INM offices inside Mexico do have the right to request updated financial information, and they occasionally exercise it. It is smart to have recent statements available just in case, even if they are not formally required.

Frequently Asked Questions

Do I need a Mexican bank account before I apply for residency?

No. Most Mexican banks will not open an account for you until you have a valid resident card, so this is not possible for most applicants anyway. You use your US or Canadian bank statements for the consulate application, then open a local account after your residency is approved and your card is issued.

What is the difference between the bank statements I submit to the consulate and what I need to open a Mexican account?

For the consulate, you need full detailed statements covering six to twelve months, showing consistent income or sufficient savings. For opening a Mexican bank account, you present your passport, resident card, proof of address, and CURP. The consulate submission is about proving financial solvency. The bank account opening is about identity verification and local residency confirmation.

Can I use statements from multiple accounts to meet the financial threshold?

Yes, most consulates allow you to combine statements from two or more accounts to demonstrate total monthly income or aggregate savings, as long as all accounts are in your name and none are cryptocurrency accounts. Check with your specific consulate to confirm their policy on combined account submissions.

Do my bank statements need to be translated into Spanish?

Not for the consulate stage, where you are submitting from outside Mexico and consulates typically work with documents in English. However, if you are completing any part of the process at an INM office inside Mexico, including the canje process, your financial documents must be translated into Spanish by a certified translator.

What happens to my bank statement requirement if I apply as part of a couple?

If you and your partner are applying together using a joint account, you only need to meet the financial threshold once for the household. You do not need to show double the required income or savings. This applies whether you are pursuing temporary or permanent residency together.

Do I need to resubmit bank documents when renewing my temporary residency?

Typically no. Temporary residency renewals do not require you to reprove economic solvency as a standard step. That said, INM offices can request recent bank statements at their discretion, so keeping updated statements on hand is a good habit even during renewal years.

Ready to Start Your Mexico Residency?

Reloca handles everything for you, from apostilles and document prep to your consulate appointment and INM filing in Mexico. Most clients get their resident card without a single stressful moment.

See our plans and get started today.